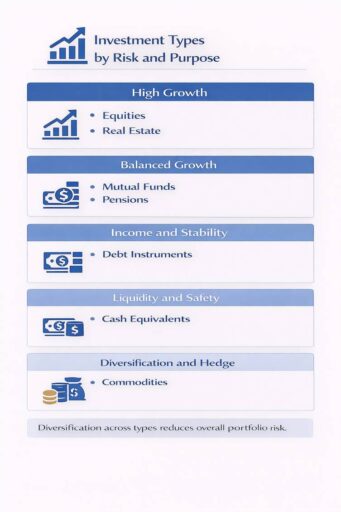

The seven main types of investment are equities, debt instruments, mutual funds, real estate, cash equivalents, commodities, and pensions.

Each category has a different risk, return, and liquidity profile, and is used differently depending on financial goals and time horizon.

This article covers:

- What is an investment asset class?

- What do you mean by equity?

- What do you mean by debt instruments?

- What do you mean by mutual funds?

- What do you mean by real estate investments?

- What do you mean by cash equivalents?

- What do you mean by commodities?

- What do you mean by pension?

Key Takeaways:

- Equities offer ownership and growth; debt instruments offer stability and income.

- Diversifying across investment types reduces portfolio risk significantly.

- Cross-border investors face different tax, access, and regulatory environments.

My contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837 if you have any questions.

The information in this article is for general guidance only. It does not constitute financial, legal, or tax advice, and is not a recommendation or solicitation to invest. Some facts may have changed since the time of writing.

What are the investment asset classes?

Investment asset classes are broad groupings of financial instruments that share common characteristics and are subject to related risk factors.

The three traditional asset classes are equities (stocks), fixed income (bonds), and cash equivalents.

Beyond these, real estate, commodities, mutual funds, and pensions form the extended framework that most globally diversified portfolios are built on.

Each class behaves differently in terms of risk, return, and liquidity.

What are equity investments?

Equity investments represent ownership in a company.

When you buy equity, you become a part-owner of that company.

Your returns come from capital appreciation (the share price rising) and, in some cases, dividend income.

Equity investments carry higher risk than debt because shareholders are last in line in the event of company insolvency.

How does equity investment work?

Equity works by allowing investors to buy shares in a publicly listed or private company, then benefit as that company grows in value.

Gains are realised when you sell at a higher price than you paid, or through dividends distributed from company profits.

There are two main equity types:

- Common stock: Full ownership rights and voting rights; dividends are variable

- Preferred stock: Fixed dividend priority, but typically no voting rights

For cross-border investors, equity returns are often subject to withholding taxes in the country of the company’s domicile, and then again in the investor’s country of residence.

Double taxation treaties (DTTs) can reduce this burden, but rules vary significantly. Always verify your tax obligations before buying international equities.

What are debt instruments?

Debt instruments are fixed-income investments where investors lend money to a borrower in exchange for regular interest payments and the return of principal at maturity.

They include government bonds, corporate bonds, treasury bills, and certificates of deposit.

They are generally used to provide income stability and reduce portfolio risk.

How do debt instruments work?

A debt instrument works as a formal lending agreement.

The borrower issues the instrument (a bond, for example), promising to pay interest (the coupon rate) at set intervals and return the face value at the end of the agreed term.

Key factors that determine a debt instrument’s return and risk:

- Credit rating: Higher-rated issuers (like government bonds from stable economies) pay less but carry less default risk

- Maturity: Longer-term bonds typically offer higher yields but more interest rate sensitivity

- Coupon type: Fixed coupons provide certainty; floating coupons adjust with benchmark rates

Government bonds from stable sovereign nations (US Treasuries, UK Gilts, German Bunds) are considered among the safest investments globally.

Corporate bonds offer higher yields but carry issuer-specific risk.

What are mutual funds?

Mutual funds are pooled investment vehicles that collect capital from multiple investors and deploy it across a diversified portfolio of assets.

They may hold stocks, bonds, money market instruments, or a combination.

They provide diversification without requiring direct stock selection.

How do mutual funds work?

Investors purchase units in the mutual fund rather than individual assets, and the unit value changes based on Net Asset Value (NAV).

Returns come from capital gains, dividend distributions, or interest income passed on to unit holders.

Common mutual fund types include:

- Equity funds: Invest primarily in stocks; suited to growth-oriented investors

- Debt funds: Invest in bonds and fixed income securities; suited to conservative investors

- Balanced or hybrid funds: A blend of equities and debt for moderate risk profiles

- Index funds: Passively track a market index (e.g., S&P 500) with lower management fees

For international investors, fund domicile is important because it affects tax and access.

For example, UCITS funds in Ireland are widely accessible and tax-efficient, while US-domiciled funds may trigger estate tax issues for non-US investors.

Fund structure and jurisdiction directly affect investment outcomes, especially in cross-border portfolios.

What are real estate investments?

Real estate investments involve allocating capital into physical property or property-linked financial instruments.

Real estate behaves differently from financial assets.

It is tangible, illiquid, and heavily influenced by local market conditions, interest rates, and government policy.

How does real estate investment work?

Real estate investment works by generating returns through two primary mechanisms: rental income from tenants and capital appreciation as property values rise.

Direct property investment involves purchasing residential, commercial, or industrial properties.

Investors earn monthly rent and benefit when the property is sold at a higher price.

Costs include maintenance, property taxes, insurance, mortgage interest, and vacancy periods.

For those who want real estate exposure without owning physical property, two accessible alternatives exist:

- REITs (Real Estate Investment Trusts): Companies that own income-generating real estate and trade on stock exchanges like shares. They must distribute a significant portion of income as dividends, offering regular cash flow.

- Real estate funds: Pooled vehicles that invest in multiple property assets, providing diversification within the asset class.

For expat investors, taxation and ownership rules vary by country.

Some countries restrict foreign property ownership, and rental income is usually taxed where the property is located.

Capital gains tax rules differ widely, and exemptions for residents often do not apply to non-residents.

What Are Cash Equivalent Investments?

Cash equivalents are short-term, highly liquid financial instruments that can be converted to cash quickly and with minimal loss of value.

They are considered the most conservative investment type and are mainly used to preserve capital, maintain liquidity, and bridge funds between investments.

The most common cash equivalents are instruments with maturities of three months or less.

Examples include:

- Treasury bills (T-bills): Short-term government debt issued at a discount to face value

- Money market funds: Daily liquidity pooled funds

- Certificates of deposit (CDs): Fixed-term bank deposits

- Commercial paper: Short-term corporate debt

- Savings accounts: The most basic form; government-insured

How Do Cash Equivalents Function?

Cash equivalents prioritize capital stability and liquidity over returns. They are used for emergency funds, short-term cash needs, and temporarily holding capital during market volatility.

The trade-off is low risk and low return, and inflation can erode real value over time.

Because of this, investors should only hold amounts that match short-term liquidity needs.

For internationally mobile investors, currency choice matters, as holding cash in a weakening currency reduces real value even if interest is earned.

What Are Commodity Investments?

Commodity investments involve exposure to raw materials and natural resources, such as physical goods whose prices are driven by supply and demand dynamics in global markets.

They are divided into three main categories: energy (crude oil, natural gas), metals (gold, silver, copper), and agricultural products (wheat, corn, soybeans, cotton).

How Do Commodities Work?

Commodities provide returns through price movements in global markets, acting as both speculation vehicles and portfolio hedges.

Investors access commodity markets through several methods:

- Physical ownership: Buying gold bars, silver coins, or other tangible assets directly

- Futures contracts: Agreements to buy or sell a commodity at a predetermined price on a future date, which are used by sophisticated investors and institutions

- ETFs and mutual funds: Commodity-linked funds that track prices without requiring physical storage

- Commodity-linked stocks: Shares in companies that produce, mine, or refine commodities (e.g., oil producers, gold miners)

Commodities are often used as inflation hedges, as assets like gold tend to retain value when currencies weaken.

However, commodity prices are volatile and highly sensitive to geopolitical events, weather, currency movements, and global demand.

They work best as asset diversification tool, not as a standalone portfolio.

What Is a Pension?

A pension is a long-term savings and investment arrangement designed to provide income during retirement

It is one of the most tax-efficient investment vehicles available in most countries, with contributions often receiving tax relief.

How Do Pension Schemes Work?

A pension scheme allows individuals and employers to contribute during working life, with funds invested to grow until retirement.

There are two primary types:

- Defined Benefit (DB): The employer guarantees retirement income and bears investment risk.

- Defined Contribution (DC): The retirement income depends on contributions and investment performance.

Most private sector workers are now in DC schemes.

Contributions are invested into selected funds, and the accumulated value is later used to buy an annuity, provide drawdown income, or both.

How Do Pension Funds Work?

Pension funds pool and manage contributions from members and invest them across equities, bonds, real estate, infrastructure, and other asset classes.

They are among the largest institutional investors in global markets.

For individuals, contributions are invested into a portfolio aligned with their risk profile and retirement timeline.

The value grows over time through investment returns and compounding, and is later converted into retirement income or withdrawals.

For internationally mobile professionals, pension rules vary by country, and contributions may not always be transferable.

Tax treatment and transfer rules also differ, making international pension planning more complex than domestic planning.

FAQs

Which investment gives the highest returns?

Over long-time horizons, equities have historically generated the highest returns among mainstream asset classes.

Commodities like silver surged 146% in a single year (2025), but such gains are rare and irregular.

High returns are always accompanied by higher risk and volatility.

Are cryptocurrencies considered assets?

Cryptocurrencies are increasingly recognized as a distinct asset class by regulators and institutional investors, though classification varies by jurisdiction.

They are high-risk, speculative instruments and carry significant volatility, regulatory uncertainty, and custody risk.

How to diversify investments for beginners?

Start by spreading capital across at least three asset classes, for example, equities, bonds, and cash equivalents.

Within equities, use mutual funds or ETFs to diversify across geographies and sectors rather than concentrating in individual stocks.

Increase real estate and commodity exposure gradually as portfolio size grows.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.