I often write on Quora.com, where I am the most viewed writer on financial matters, with hundreds million views in recent years.

In the answers below I focused on:

- Is art a good asset class for an investment portfolio? I look at the negatives associated with it but also one of the huge innovations of recent times, which could make it a more attractive asset class going forward than previously was the case.

- How much do you need to be considered a high-net-worth individual (HNWI)?

- Why should all good investing be boring?

- Is investing in the Chinese markets, and entering market bonds, really becoming more important for investing houses?

Some of the links and videos referred to might only be available on the original answers.

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Is art a good asset class for an investment portfolio?

Source: Quora

This has changed over time. Recently there has been a game changing development.

I will get into what has changed later on in the answer.

Anyway, in the traditional sense of the world, art hasn’t been a great investment.

The main reasons have historically been:

- The costs of storing and insuring the art have traditionally been astronomical. This decreases the net returns.

- It is hard to find a buyer for many pieces of art. Like watches and other collectables. it hasn’t historically been as easy as selling an ETF

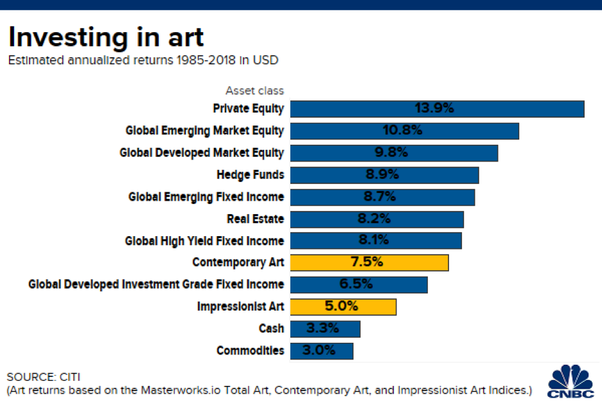

- It hasn’t done as well as the S&P500. Now sure, it has done better than most collectables. It also depends on when you buy. There have been some periods of time when it has beaten stock markets but it hasn’t on average:

Remember too that if you include the storage and insurance costs, those figures will change dramatically.

You can buy an ETF from 0.1% per year. Traditionally it has cost 2%-3% to store and insure art.

In previous decades the difference between art and stocks was even bigger.

The reason is pretty simple to understand. Art is a collectable. Fine art doesn’t dramatically go up in terms of supply, and demand fluctuates.

Demand tends to be relatively stable and sometimes shoots up if you get new discerning consumers in newly rich countries, but over a long period of time (say 50 years) demand doesn’t usually skyrocket.

In comparison, stocks pay a dividend and the capital growth is high.

If you buy the S&P500 you are buying 500 of the most innovative firms in the world.

Those firms will change over time due to the social darwinism that exits.

Therefore, we can’t predict which firms will be on the index, but we sure as hell understand that the most profitable firms in 2050 will be more profitable than 2021 due to new technologies and innovations.

So, the bottom line is, art has always been more costly to own, more risky in terms of finding a buyer, and has less upside than an asset class like stock ETFs.

Remember, something has changed recently. Digital art now removes the need to insure and store art.

This means that the gross, and net, performance will be similar, unlike the way most people buy art.

Despite this, I still don’t expect digital art to be the best performing asset class in the next 100 years, but it will almost for sure outperform the traditional way of buying it.

This trend towards storing digital assets will affect plenty more assets as well.

I was watching a video a few days ago where the presenter was mentioning how 12-year-old kids who are into video games, are trading digital swords and all kinds of “assets”.

I think this kind of trend will also start to affect watches and other assets which have traditionally been expensive to keep.

How much is one considered an HNWI (high net worth individual) in the wealth management industry?

Source: Quora

Now this is a great question because whilst definitions are sometimes pointless, here they aren’t.

Investopedia’s definition is quite common “A high-net-worth individual (HNWI) is somebody with around $1 million in liquid financial assets. HNWIs are in high demand by private wealth managers. The more money a person has, the more work it takes to maintain and preserve those assets”

Ultra-high-net-worth is usually $30m or above in liquid financial assets.

The key word here is liquid. How easy is it to sell the asset? A property, especially a primary residency, isn’t liquid.

A business isn’t liquid either. It is even harder to sell than property quickly.

It can take years, decades or sometimes you will never find a buyer.

Therefore, we can’t compare somebody who has $1m invested in stock ETFs to somebody with a private (unlisted) business, or a primary residency.

For me, I would argue that a distinction also needs to be made between somebody with rental property vs a primary residency.

In many ways, a primary residency can be a liability. Even some professional real estate investors I know rent but buy properties on the side.

They understand a simple truth. Rental properties put money in your pocket regardless of whether they are the best investments or not.

A primary residency can sometimes be cheaper than renting and it does sometimes make sense to buy rather than rent.

However, in some situations, it takes money out of your pocket. If you “rent low but buy high”, in other words buy the biggest possible property you can afford, the bills, taxes and maintenance costs are super high.

What’s more, even if it goes up in value, it is only one house. You might die in it, and your kids will inherit it.

So, unless you plan to downsize in retirement and use the surplus money, you don’t even benefit from the increase in capital values.

So here is the thing. If somebody is worth $5m, and $800,000 is in liquid assets and $4.2m in rental properties, an argument can be made that they are high-net-worth.

In comparison, if somebody is worth $5m on paper, but almost all of that is kept in a primary residency, then they aren’t HNWI.

In fact, they might be struggling to keep up with the mortgages payments.

Some of these people are even quite poor and struggle financially, because they have got it into their mind that taking out a huge mortgage will eventually pay off.

These people are now called “house poor”:

For me, a simple rule of thumb is to ask this question – “how many pay cheques could you live from if you got sick tomorrow and needed to retire due to illness”.

If the answer is that you could only live for a few months unless you found a buyer for your business or house, then you might have paper wealth, but you aren’t that secure.

If you could live forever from a liquid portfolio, even if your net worth isn’t super high, then there is a strong argument to say that is a HNWI.

Covid-19 has shown the importance of liquidity. Those who had 100% of their eggs in one illiquid basket (like a primary business or residency) often regret it during the hard times.

I like to invest, but I’m getting sick of stocks and bonds. What are some other things I can invest in?

Source: Quora

I am going to tell you such a simple tip now. In investing, boredom is a good thing.

Soros has it right here:

For the average investor, boring investing is even more important, because most people don’t have the specialized knowledge to get into new asset classes, or have access to advisors.

Buying and holding safe assets long-term, and automating the process by direct debit, is therefore one of the best things you can do.

There are other investments you can go into though such as

- Real estate investment trusts (REITS). An easy way to own real estate without all the costs and hassles of direct property.

- Direct/traditional real estate through buying rental property.

- Private equity or angle investing if you are high-net-worth.

- Other professional type asset classes like structured notes

- Gold and silver

- Industrial commodities such as cooper, oil, gas, coin etc. These can be bought through ETFs like gold and silver can these days.

- Collectables such as art, watches, stamps, antique furniture, comic books etc.

- Corporate bonds assuming you meant you only own government bonds in your answer.

- Cash-like assets like t-bills

- A business. In other words, starting your own business.

Yet almost all of those assets, apart from REITS perhaps, are either

- Much riskier than what you seem to be doing

- Take a lot of time and time is money

- Lower yielding than stocks in particular.

- Only available to high-net-worth investors in some countries due to regulations.

- Cost more money to gain access to

- A combination of all of the above or require specialist knowledge to do it safely.

I would just stick to what you are doing or gradually learn about these new asset classes, and allocate 5%-10% of your portfolio to it.

What I would do, however, is look more closely at your stock:bond ratios. Bonds are very low-yielding these days.

They shouldn’t be ignored but I do think you don’t need a high allocation to them when you are young.

They become more important close to retirement.

Why have emerging market bonds or Chinese stocks become important in major investment houses today?

Source: Quora

Well I am not sure they have become that important to most major investment houses compared to a few years ago.

I would make one comment though – both asset classes look undervalued and yet risky in some ways.

The Chinese Stock Market, the Shanghai Composite, was one of the best performing investments in the 1990s and early 2000s.

It has been one of the worst performing stock markets in the last fifteen years in the world, despite the ups as well as downs.

If you look at the market from a P/E and Cape basis, it looks cheap compared to what it was before, and also versus some other International markets.

The quote below is very true in investing, so I am sure the Chinese market will have its day in the sun one day:

Yet remember that markets aren’t stupid, even if they aren’t always efficient.

Investors rightly perceive the Shanghai, and indeed Shenzhen, markets to be riskier than US and some other stock markets.

The same thing is true of emerging market bonds/debt. In a world where US Treasuries pay so little, and so do other developed market bonds, there is a place for emerging market debt in a portfolio.

Considering the risk you would need to take to get higher returns, however, it doesn’t seem worthwhile to invest in this form of fixed income, unless it is a small part of a larger portfolio.

What has been the case for a long time is that Chinese stocks have been part of MSCI World and indeed MSCI Emerging Markets, even though China is now a mid-income country.

That means many investors are exposed regardless of whether they intended that or not.

The same thing is true of emerging market debt. If you buy a global bond fund, by definition you will get an allocation to emerging market debt.