I often write on Quora.com, where I am the most viewed writer on financial matters, with over 491.7 million views in recent years.

In the answers below I focused on the following topics and issues:

- What are 10 questions to ask yourself before investing a penny?

- How does inheritance tax in the UK work?

- For non-US markets, how well does the Shiller’s CAPE ratio predict long-term stock market returns?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

Some of the links and videos referred to might only be available on the original answers.

Source for all answers – Adam Fayed’s Quora page.

What are 10 questions to ask yourself before investing a penny?

Keeping it to ten is difficult but I will make a stab at it.

- Do I need an emergency surplus of cash in case I lose my job? If so, do I have 3-6 months of living expenses saved up?

- What do I need beyond pure investing advice? For example, if you are an expat you might need account portability as you are moving around. Or if you are high-net-worth you might require inheritance tax planning.

- Do I understand the investment, or have somebody (like a consultant or advisor) who does?

- Do I often get influenced by the views of the news media, friends and family? Will I therefore panic if markets go down?

- Following on from the last question, do I therefore need an investment advisor to control my emotions as much as for knowledge?

- Am I comfortable with volatility because risk and volatility aren’t always the same thing.

- What am I investing for? A medium-term objective, or something like retirement? If it is short-term, it is best not to invest in most kinds of stock assets, as they are best left as long-term investments.

- How much risk do I want to take?

- How much risk am I taking now by leaving money in cash, due to the threat of inflation and currency falls?

- Is my attitude to any of the above sensible? For example, am I too risk-adverse or want to take too much risk?

However, I would say one of the biggest mistakes people make is overthinking things in the first place, and asking too many questions.

As per this quote, most of life is about showing up:

It is better to get started today with 80% certainty than wait for 99%, as that never happens.

That is one reason people tend to “think about” investing for months, years and even decades!

Subsequently most regret not getting in sooner.

How does inheritance tax in the UK work?

Some British expats living overseas will probably be amazed by my answer.

This is a potential tax trap, which I will deal with later in the answer.

Firstly, let’s focus on people living in the UK.

For people living in the UK it is quite simple. 40% on anything above £325,000. So, if your estate is worth £1,325,000, you pay tax on a million and not the 325,000.

Of course, there are things people can do to minimize it such as:

- Taking advantage of gifts and reliefs. For example, you can pay 3,000GBP per person, per year, tax-free.

- You can give gifts, tax-free, when somebody marries. It is currently £5,000 to a child, £2,500 to a grandchild or great-grandchild and £1,000 to any other person. So, in a year where your child gets married, you can give 8k tax-free.

- There is no tax on certain kinds of gifts if they are given seven years before death.

- There is business relief for owners of companies

- You can set up trusts.

The devil is in the detail, and those details always change, so needless to say this isn’t formal tax-advice, and it does pay to get advice from a tax advisor and/or do your own research.

Yet the more striking aspect of inheritance tax is for those living overseas.

Many British people mistakenly think that just because they have changed their residency, tax residency or even citizenship, that this means they don’t need to pay the 40%.

Just because somebody lives overseas and has no UK tax ties and therefore doesn’t pay UK income taxes, doesn’t mean that inheritance taxes works in the same way.

Residency, tax residency and domicile work differently. Domicile is the hardest thing of all to change.

So, you could have not spent a day in the UK for fifty years but still pay 40% on assets above 325k, no matter where the assets are located globally.

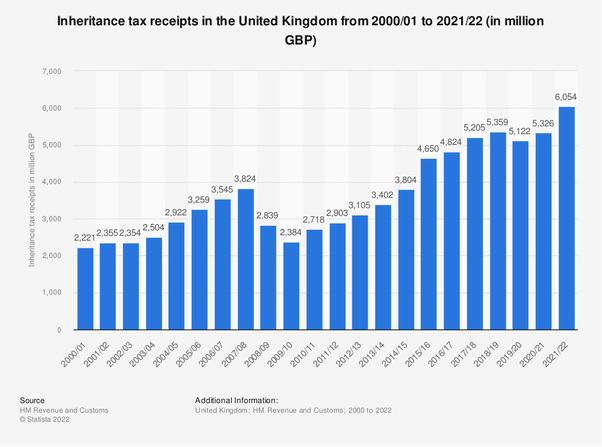

No wonder UK inheritance tax receipts are hitting records. I doubt it is just because of higher levels of wealth:

In a post-Covid era, where governments need more tax money, the rules will probably get harsher.

The good thing is people living overseas have access to offshore trusts and other legal structures, which makes effective inheritance tax planning possible.

For non-US markets, how well does the Shiller’s CAPE ratio predict long-term stock market returns?

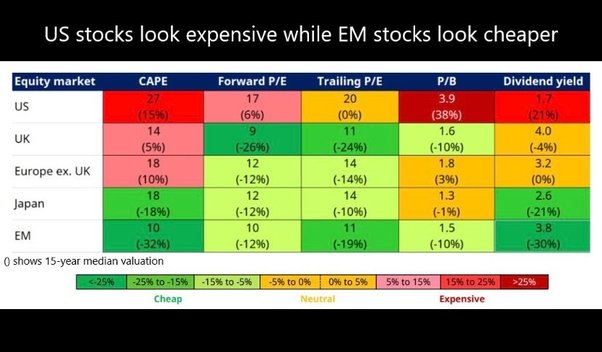

If we look at the graph above, the current CAPE ratios show that the UK, Japanese, European and especially emerging markets look cheap.

That has resulted in many people asking the same question that has been asked here.

Ultimately, there is no perfect way to predict markets. If there were, everybody could market time. I have yet to meet a person who has kept money in cash, hoping for a fall, to beat the stock market consistently.

Having said that, the CAPE ratio is as good a measure as any in terms of predicting the next decade or two for a given market.

It is certainly better than:

- The rate of inflation.

- Which political party will win the next election.

- If a war will happen

- If the economy is super strong

- Geopolitical conflict

- Pandemics

- Almost every other single measure the media speaks about in a misleading way.

- It is even better than simple price:earnings ratios

The markets have done well, and badly, under all of these conditions. They went up during the Cuban Missile Crisis, WW1 and the Spanish Flu pandemic and the recent Covid-19 episode.

So, the CAPE ratio is a better valuation measurement than most.

What is even better is this. Not comparing CAPE ratios by market, but comparing the CAPE ratio to its historical levels.

For example, comparing the Hong Kong market’s CAPE to its historical level, rather than to the S&P500 or FTSE100.

It is still an imperfect measurement. The Russian stock market looked cheap for a long time, but we now understand that buying it would have been a mistake.

We also have to factor in risk. Emerging markets are riskier than US stock markets.

Buying country-specific funds and ETFs is just a slightly easier way to beat the S&P500, compared to stock picking.

One reason is that few individuals or even institutions want to buy unfashionable investments which haven’t performed well for a long time (those firms with low CAPE ratios).

People prefer to buy emerging markets when everybody else is (the 2000s), and not when they have underperformed US markets for over a decade (now).

Likewise, everybody loved technology in the late 90s, but not in 2002.