I often write on Quora.com, where I am the most viewed writer on financial matters, with over 270.1. million views in recent years.

In the answers below I focused on the following topics and issues:

- What are the riskiest types of investments? Bonds, stocks, options, futures or real estate? Or perhaps that is the wrong way to look at the question, and we should instead focus on our investing behaviour, such as how long we invest for? I explain how we can lower investment risks, and be investors rather than speculators.

- Many people are interested in fast growing markets in South East Asia. Therefore, many people ask how you can invest in Myanmar’s future? Is investing locally the only option? I suggest why investing internationally in assets such as MSCI World and the S&P500, can indirectly benefit you, even if far flung economies do well.

- Can we know, with any degree of certainty, when the US stock market will next crash? What does recent history tell us about how predictable the stock market really is?

Some of the links and videos displayed on the original answers might not show up on here, and if so, you will need to refer to the original answers to view that.

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me, email (advice@adamfayed.com) or use the WhatsApp function below.

What are the riskiest types of investments?

Source: Quora

The riskiest type of investment is something which is completely based on speculation.

An example is buying and selling assets which don’t go up in value.

For example, currency trading. The Euro can’t go up against the USD at the same time as the USD goes up against the Euro:

You don’t even make any money in the bank holding them.

Therefore, it is all about timing, and 99.9% of the people engaging in this activity are speculating.

Stock trading is also risky compared to buying and holding stocks.

It is less risky than currency trading because the base asset (stocks) do go up in value over time.

Not every stock, but the entire stock market. They also pay dividends so if you sell out and make a loss, you still get the dividends.

Yet if you buy and sell them on a daily or monthly basis, you are still speculating.

Amazon can’t beat the market at the same time as Amazon loses to the S&P500.

That means that one person is on the losing side of the trade and the other is on the winning side of the trade.

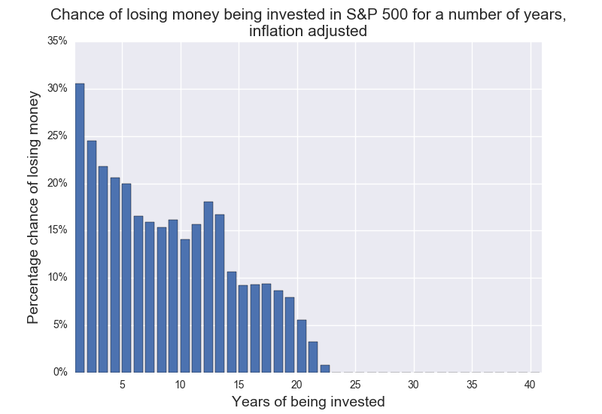

In comparison, if two people both hold the S&P500 or MSCI World index for decades, both people will win.

In fact, both people will get the same percentage return, if they bought at the same time.

Indeed buying stock indexes for long periods of time isn’t speculative as shown by the below results:

We can also see the same thing in real estate. Flipping real estate (buying and selling quickly) can be profitable as can stock trading, but it is more of a speculation.

Buying and holding real estate in the hope that somebody else will buy the same asset later on for more (capital appreciation) is a form of speculation as well.

In comparison, focusing on what the asset actually yields (the yield) is less speculative.

The biggest signs of a speculative vs an investor is:

- They are focusing on hot ideas

- Short-term orientated rather than focusing on the long-term

- Trying to buy and sell, and market time, as opposed to buying and holding

- Not focusing on diversification at all

- More obsessed with capital appreciation if they are buying property rather than the yield

- An obsession with stories and personalities, like who the CEO is

- Needing to feel like investing is exciting. Good investing can be very boring.

So, often it isn’t the asset itself which is risky. People get this wrong.

It is how you use the asset. Buying one stock for a year is super risky, as is trading stocks.

Buying and holding an entire market like the S&P500 for decades isn’t risky.

The same is true in private business. People say starting a business is risky.

That is usually true, but starting one without experience and focusing on debt/leverage is very risky.

Only starting a business after having years of experience in a domain isn’t nearly as risky.

There are some assets which are risky for all non-professional investors, like options, but few people use them.

What are the best ways to invest in Myanmar’s future?

Source: Quora

Most wealthy local people are trying to do the opposite – take money out of the country.

I am not saying the country doesn’t have potential. Barely a few years ago a lot of hot money was coming in from nearby countries.

Many multinationals were trying to get in early as well. Things have changed a bit now due to the political situation.

Also remember this. Let’s say Myanmar gets pasted this recent issue, which is a very real possibility.

Even in a best case scenario, the same thing will happen with Myanmar as has happened in places like India, China and Vietnam.

Namely, some of the best local firms will IPO in the United States and maybe Hong Kong and beyond.

So, I wouldn’t invest locally in the country, in local real estate or the stock market.

The risk:return ratio isn’t great. I would just be globally diversified and you will naturally get the benefit of any huge growth.

Think about it this way. Come 2050, if Myanmar is a huge success story, MSCI World will be full of local firms from the area, and even the S&P500 might have one or two companies which started out locally.

Remember what happened with China. Most of the non-Chinese who have made the most money have just benefited from more Chinese firms doing IPOs on the US stock market.

The people I know who tried to get access to Chinese growth locally had very mixed results.

I am not saying the same thing will happen here, but in a global world, it is possible to get access to growth markets without physically putting money into local markets.

Even if you want something which is a bit more “South East Asian centric”, you can buy a SE Asian tracker/index funds, which tracks all the markets in the region.

If you do this, firms from Myanmar will become more prominent if they succeed, and less prominent if the economy becomes weaker, as most of these funds and ETFs distribute allocations by the size of the GDP.

In other words, the likes of Indonesia and Thailand have a bigger allocation compared to say Laos which has a small GDP.

In any case, emerging markets aren’t a free lunch. They have a lot of risk, often for little reward vs developed markets in the long-term.

When is the US market crashing next?

Source: Quora

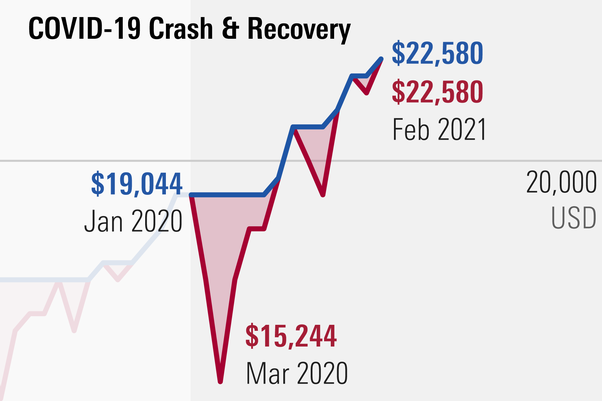

Consider this. Last February or March, few saw the crash coming, especially a global one.

There were people who were predicting a US stock market crash, but very few predicted a global crash, including those undervalued European and Emerging Markets which had struggled for years and had low p/e ratios.

Then stocks crashed. The few people who predicted it felt smug. Yet very few of them predicted the upswing:

What is more, most of the (few) people who correctly predicted the 2020 crash also predicted that markets would crash in 2019, 2018, 2017, 2016, 2015 and every year before that.

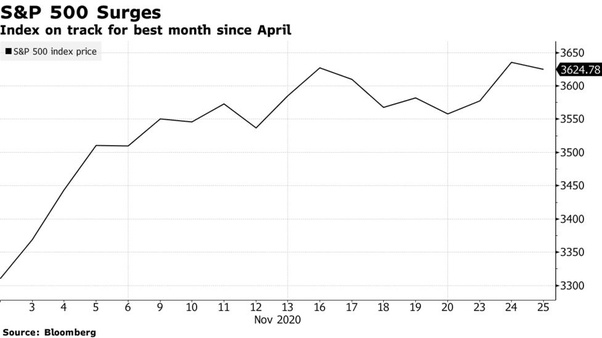

Few, if any, took advantage of the falls, and most also predicted a US stock market crash in November if there was a disputed US election which would add uncertainty.

There was a disputed US election, which happened during a second European lockdown.

What happened…..markets surged!

Just as markets had unexpectedly surged after Trump’s 2016 victory, markets went up even before the vaccine was announced.

In fact, they went up on the day after the election, and the day after that as well.

What I have learned down the years is rather simple

- Those who predict one crisis correctly, get the next one wrong. Past predictions are no indication of future right ones

- Predicting the end of the world isn’t very profitable

- Markets always come back even if individual stocks and sectors (like the banks after 2008) don’t.

- 90% of people who wait for a stock market crash, end up waiting for an even bigger one, and never get in. All those people who thought the Dow would go down further than 17k are often still in cash.

- The same people who predicted that markets would go down during the 2016 election thought the same thing in 2020 and no doubt they will make the same mistakes again in 2024 and 2028. If they finally get one right, they will boast about the right prediction

- It just isn’t profitable to try to predict the future compared to investing for the long-term now. The people I know who have made the most from markets have invested for decades and forget about it

- The media makes more money from negativity and doom and gloom than optimism, so they will always predict that “this time is different”.

- People go from one extreme to the other. This time last year people were worried about a Great Depression. Now some of the same people worry about an overheating economy and inflation! The same people worried about huge inflation in 2009 after QE are worrying again.

- Controlling your emotions is much more important than technical knowledge in investing. I even know some finance pros who panic sold during 2020, even though they know it doesn’t make sense. Studies show that 35% of people in DIY brokerages panic sold, with more playing the wait and see game (not adding more money). Only a minority of people had a plan, like invest every month through rain and shine, and stick to it during the bad periods.

- Net buyers of units (younger people and even some middle-aged people) should celebrate crashes. That doesn’t mean staying in cash. It just means that if markets stay low for years, you can buy more units. For example, the best time for a young person to buy stocks would have been the “lost decade” from 2000 until 2010. Few think that way though. Only net sellers (those in retirement) should worry about crashes, but by that point you shouldn’t be 100% or even 90% in stocks anyway. Even a retiree with a 70%-30% or 60%-40% portfolio, doesn’t need to worry about crashes.

- People who have seen it all before get so fed up with explaining that you shouldn’t time markets, that the only people shouting about potential crashes are the kinds of people who shouldn’t be taken seriously.

- Having a simple, long-term strategy, will eventually beat more complex ones for most investors.

The bottom line? Don’t try to time markets. Just invest now with sensible asset allocation, and forget about it.

If it was easy to predict the future, then everybody would have bought during the 2000, 2008 and 2020 dips.

Further Reading

In the article below, taken directly from my online Quora answers, I spoke about the following issues and subjects:

- Is there an index fund for South East Asia companies like Vietnam, Thailand? If so, is investing in such a fund a good idea?

- What would I do if I was given $1million tomorrow? Would I spend it, invest it or do both?

- How can human nature actually help us save and invest more? I discuss some of the simplest strategies for saving more without trying.

- What kinds of assets do high-net-worth individuals invest in apart from stocks and real estate? Does it matter how the person got wealthy to begin with?

- How can people invest in US stocks from Ghana? Do most people need advice and guidance?

To read more click on the link below.