In this blog I will list some of my top Quora answers for the last few days.

In the answers shared today I focused on:

- Can somebody on a middle-class income become rich or wealthy, or is it unrealistic?

- Do annuities offer good value for money or is drawdown superior for retirees?

- Are house prices likely to go down next year across the board, or will there be a shift in terms of house price inflation? More specifically, I investigate whether prices will rise substantially outside of big cities now more people can work from home.

- Is there such a thing as the safest company in the world to invest in? If not, what is the safest strategy in the investing world to reduce your risks of loses?

If you want me to answer any questions on Quora or YouTube, or you are looking to invest, don’t hesitate to contact me or use the WhatsApp function below.

Are middle class actually able to become rich by stock market?

Source: Quora

It depends how you mean by rich. if you mean hundreds of millions or billions, then it is very unlikely.

If you mean become a millionaire or multi-millionaire then it not only can be done, but many wealthy people took this route.

In this book below, the authors tried to answer a simple question.

Has the world changed since the Millionaire Next Door was produced?

So, it might not be as famous as the Millionaire Next Door, but the Next Millionaire Next Door is more updated.

They looked at wide data pools, and found that whilst a few things might have changed, most wealthy people are middle or upper-middle income.

They had certain things in common like living below their means and investing the surplus well.

Therefore, in most developed and high-income countries at least, there are a lot of middle-aged and middle-class multi-millionaires.

Of course, most middle-income people don’t reach that point, but that is usually because of the following reasons:

- Unexpected events – divorce, long-term unemployment and ill health at a young age

- Bad spending habits – no matter how much or little you earn you need to generate a surplus to invest

- Not being long-term or patient enough – Investing for 5–10 years isn’t the same thing as 40 years.

- Panic selling when markets are crashing – It happened in 1987. It happened in 2000 and 2008. it happened again in 2020. Many people get in when markets are soaring (fear of losing out/greed) and panic when markets are falling (fear). What is more key is just investing through thick and thin. Often people do this after getting scared after speaking to friends or family, or listening to the media. What doesn’t help is some “experts” give misleading advice. Take this guy who wanted against buying giving covid even when the Dow was at 17k- ‘This is different’ — El-Erian warns against buying coronavirus pullback fears in stock market . Markets have risen about 82% since his comments and numerous studies have shown that listening to the media will lower your returns – CNBC vs Bloomberg? Switch them both off

Ultimately, markets rise long-term, even adjusted for inflation. 30 years today the S&P500 was at about 330 and the Nasdaq was at 450.

Now the S&P500 is at 3,660 and the Nasdaq at over 12,000, and that isn’t accounting for dividends.

If we went back further, say to 35 or 40 years ago, the stats look even better, despite all the falls, crashes and craziness in the middle.

That means that people that are willing to invest long-term can become millionaires by investing hundreds a month for a long-time, or having a lump sum of $50,000+.

This opens up opportunities as most people, even people at the lower-middle end, often get unexpected lump sums from inheritance and other sources.

Small amounts can become bigger over time, but many people don’t have the patience and give up if markets have gone through a tough period.

What are some of the best annuities?

Source: Quora

To answer your question quickly, some of the low-cost ones offered in some countries are the best annuities for most people.

Examples include from Vanguard and some others. Yet I would make two points here:

- Various studies show that annuities offer poor value compared to drawdown in most situations. In other words, even the best value annuities are unlikely to beat just drawing down your portfolio.

- Times have changed since the 1980s, 1990s and even early 2000s and this has affected annuity rates.

Let’s deal with the second point first. Even as recently as 2000, government bonds paid 6% in many advanced countries.

Cash paid inflation +2%. Don’t get me wrong, fixed income and cash has never beaten stock markets long-term, but the gap used to be smaller.

Historically cash paid 1%-2% above inflation, fixed income +3 or 3.5% above inflation and stocks 6%-7% above inflation.

In the last 10–12 years, the gap between the performance of say the S&P500 and a more diversified index like the MSCI World, and fixed income, has grown larger.

Of course, there are various reasons for that, including the fact that asset prices were depressed after 2008.

Yet one of the biggest reasons for that is people are now searching for yield.

It is no longer possible to accept lower long-term towards, in exchange for lower volatile, by having a big percentage of a portfolio in bonds and cash close to retirement.

That has resulted in more people looking to assets that produce a yield – stocks and the real estate market to a lessor extent.

This also links to annuities. Historically, at least when interest rates and bonds rates were higher, insurance and other companies were willing to offer high annuity rates as there was a “low risk” way of earning.

Now, as mentioned, times have changed, so low interest rates are harming annuities.

That has, therefore, made annuities a poor value proposition compared to just drawing down a portfolio.

This has always been the case. Ultimately, there is no such thing as a free lunch.

A company won’t pay you a fixed income without getting something themselves.

Often they are enticing for people because they offer some kind of stability, which is ideal for people living in a low-inflation country.

The fact is that the more specific terms and conditions often mean that better options exist in the market.

Will home prices go down next year?

Source: Quora

Nobody knows for sure, especially in this climate, because a lot of governments are propping up the housing market with schemes.

What I suspect could happen is there are new trends which emerge.

In many developed countries in the last 15–20 years, big cities have done far better than smaller towns.

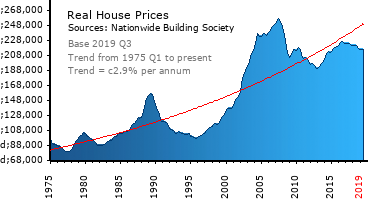

Take the UK as an example. Nationwide, UK house prices have never recovered since 2008.

In 2020, house prices adjusted for inflation are higher than in the 1980s, 1990s and early 2000s, but are roughly where they were in 2005–2006.

UK House Prices were 183,000 according to Nationwide in 2007–2008.

The same survey has them at about 220,000 now, which is a fall adjusted for inflation as the graph from House Price Crash shows:

Most people think housing “only goes up” because they don’t factor in inflation which compounds at 2%-3% per year.

The media doesn’t help with this as they often report news such as “house prices increased by 2.5% in the last year”, rather than also mentioning that is a 0% real rise.

But anyway, London house prices have bucked this trend, as have many other big cities.

In other words, prices in London, despite dipping for a few years after 2008, have hit record highs in both nominal and real inflation adjusted returns.

The world has changed now after coronavirus and was changing anyway.

So, there is a reasonable chance the opposite trend could happen in the coming decades.

In other words, big cities like NYC and London see stagnating or falling real house prices, with only rises in nominal prices, whereas cities and towns close to big cities see rises.

If we are moving into a Post-Covid world where most people spend at least a few days working from home, more people will move out of the big cities.

Again though, nobody knows for sure, because if that does happen, there will be huge political pressure to change strategies.

I can remember in 2013, the UK housing market was struggling badly.

It hadn’t recovered for years after 2008. Then George Osborne, the UK’s equivalent of a finance minister at the time, announced the “help to buy scheme”.

Essentially, the government stimulated the housing market. You can imagine that if house prices are falling for years in big cities, or even stagnating if that period of time is long, there will be a lot of lobbying to change the situation.

Lobbying already helps keep the status quo. If building on land was made easier in some countries, like the UK, you could see a “Dubai situation”.

What I mean by that is a big city which is so swamped with oversupply that prices regular fall and sometimes never truly recover.

That could also be the case for commercial property. Rents and buying prices could fall in a big way considering less big firms need so much space.

So, to answer your question, I think it will depend on government policy, and the country, city or town you live in.

What is the safest company to invest in?

Source: Quora

There is not one company which is easiest the safest. The reason is simple – the facts can change.

Firms that have a solid balance sheet today, might not have a good one tomorrow.

Look at GE. They were once so mighty that the US Government considered breaking them up on competition grounds.

That sounds similar to Amazon today! Yet in 2008–2009, they needed a bailout.

They have since returned to profit, but they are still a shadow of their former self

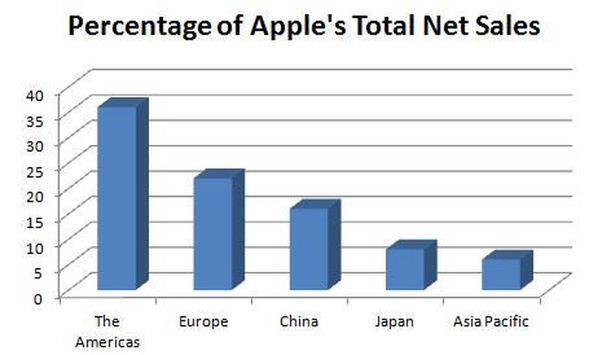

Of course companies that have diversified revenues by geography, like Apple below, are much less risky than very localized firms:

If Apple gets kicked out of China, like Facebook was, it won’t cause them to go out of business.

Likewise, if you invest in Berkshire Hathaway, you are indirectly investing in more firms than are listed on the Dow:

If you want a formula that has never failed, you need to do this:

- Invest in an index from your own country which is diversified. For example, the S&P500 in the US which 500 top companies

- An international index which covers the world

- A bond market index

Hold it long-term, reinvest the dividends and never panic sell. That has worked even for people who got unlucky.

For example, somebody who would have bought the Japanese Nikkei at the height of the bubble + an international index + a bond index would have done quite well, if they had reinvested dividends and rebalanced every year.

In fact, they would have done almost as well as somebody who was just in the S&P500 and a bond market index, because for years the rebalancing towards the underperforming market of Japan would have helped after the market picked up.

Let me give you a simple example of what I mean:

- You start with a $100,000 balance. $30,000 in bonds, $40,000 in the S&P500 and $30,000 in the Japanese Nikkei as you are a local. The next year, the Japanese Nikkei component is down to $25,000 because it has been a bad year after the bubble burst in the late 80s. The S&P500 is at $44,000 and bonds $32,000.

- Now you need to sell some bonds and S&P500 units to keep the original 30% allocation to the Nikkei, as the Nikkei has underperformed.

- As this underperformance lasted for over a decade or more until 2009, gradually you would have bought more units of the Nikkei

- In the last 12 years, the Nikkei has done almost as well as the S&P500 and better than most markets. As you have spent 15–20 years buying cheaper units by rebalancing, your portfolio would have benefited.

Of course, most people don’t need to invest in the Nikkei unless they are paid in Yen, but I gave this example to show how this strategy works even if you are unlucky enough to buy one of the worst performing indexes at the wrong time.

Further Reading

Why is discipline so important?