What Is A Bond Ladder

Understanding what a bond ladder is and how it works is key for building diversified bond investments that offer stable returns over time.

If you are looking to invest as an expat or high-net-worth individual, which is what I specialize in, you can email me (advice@adamfayed.com) or WhatsApp (+44-7393-450-837).

Introduction

Bond exposure is available to income-seeking investors through mutual funds, ETFs, and—for those with enough assets—individual bonds.

Creating a portfolio or ladder of bonds with a range of maturities is a common way to hold individual bonds.

Bond ladders are a common investment strategy used by investors to manage some potential risks associated with changing interest rates, reduce exposure to speculative stocks, and produce predictable streams of income.

What is a Bond Ladder?

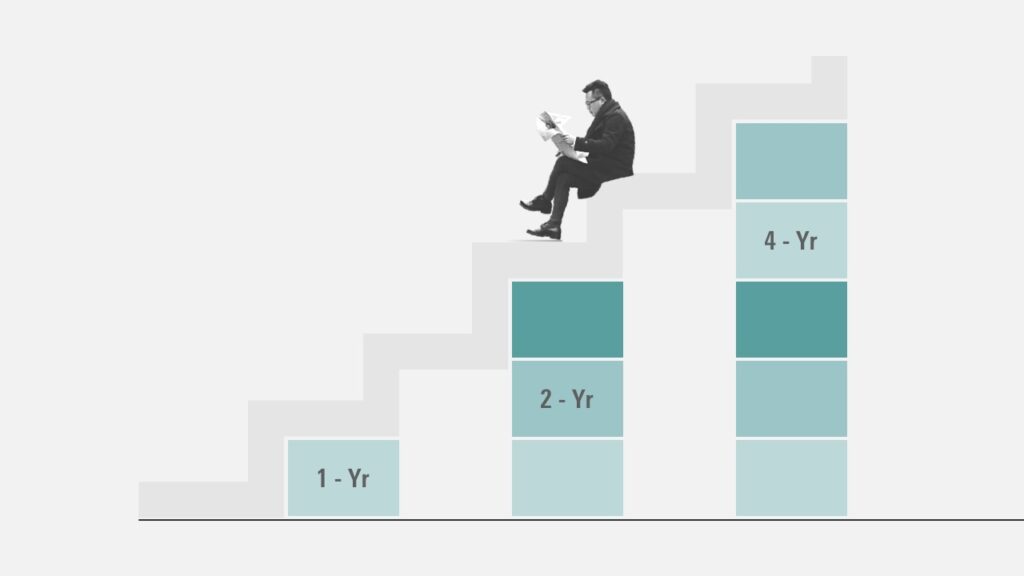

A portfolio of fixed-income securities with a significant difference in each security’s maturity date is referred to as a bond ladder.

The goal of buying multiple smaller bonds with different maturities rather than a single large bond with a single maturity date is to reduce interest-rate risk, boost liquidity, and spread credit risk.

A bond ladder evenly distributes the maturity dates of the bonds over a period of several months or years, allowing for regular reinvested distribution of the proceeds as the bonds mature.

Bond maturities should be spaced closer together the more liquidity an investor needs.

How Bond Ladder Works

A bond ladder can help you minimize interest rate risk while still generating a steady income stream. The bonds (or bond funds or ETFs) on the ladder have varying maturities.

When the ladder is first constructed, the portfolio’s bonds with the earliest maturities will typically have the lowest yields. The highest-yielding bonds in the portfolio are typically those with the newest maturities at the top of the ladder.

You have the option of reinvesting in bonds on the highest rung of the ladder when the bonds on the lowest rung of the ladder mature, or of withdrawing your investment entirely.

According to interest rates at the time you reinvest, the yields on the bonds could be higher or lower as you do so (reinvestment risk).

Your return will increase if interest rates are higher because you can reinvest at a higher rate. However, you will still have bonds at the top of the ladder that are paying higher rates, so even though interest rates are lower, your principal won’t return as much as it might.

Bond ladders shield you from changes in bond prices as well. Bond prices decrease as rates for borrowing money increase. However, the ladder is built to hold the bonds until maturity, so the strategy is unaffected by changes in the portfolio’s value.

For retirees, the strategy may be especially helpful. A bond ladder’s main benefit is greater assurance regarding the dollar amount of future payouts.

For instance, if a retiree has a set, inflexible annual spending goal for the future, they can lock in this sum by building a ladder of bonds with maturities in the years to come.

Example of a Bond Ladder

Let’s use the example of having $75,000 to invest. You could put $25,000 into a one-year bond paying 6%, $25,000 into a two-year bond paying 6.25%, and $25,000 into a three-year bond paying 6.50% to build a bond ladder. Every year is thought of as a “rung” on the ladder.

Now, you would reinvest the money from the one-year bond’s maturity into a three-year bond. You would invest the money from the matured two-year bond’s proceeds into a three-year bond at the end of the second year, and so on.

Primary Goals of a Bond Ladder

An investor can achieve two main objectives with the aid of a bond ladder.

1. Management Risk of Interest Rate

Investors can avoid being shackled to a single interest rate by spreading out maturity dates.

Depending on how many rungs there are in the ladder, there are bonds that mature every year, quarter, or month, which helps to mitigate the impact of interest rate fluctuations.

An investor may reinvest the principal of a maturing bond in a new, longer-term bond at the top of a ladder. In the event that interest rates have increased, they will profit from the new, higher interest rate and maintain the ladder.

2. Cash Flow Management

Bond income can be structured by investors to be predictable each month based on coupon payments with a range of maturity months and years. This is due to the fact that many bonds pay interest twice a year, usually on the same dates as when they mature.

How to Build a Bond Ladder

Building a bond ladder is a simple process. You can build a bond ladder with the help of a financial advisor, or you can do it yourself by following the steps listed below:

Step 1

Invest in a variety of bonds that have various maturities. The number of bonds, maturity dates, and securities you choose should be based on your financial situation and objectives.

Step 2

Hold each issue until it matures and gather interest payments as you go.

Step 3

You can decide whether to reinvest in the ladder after each bond matures or to use the proceeds in another way.

3 Fundamental Bond Ladder Ideas

Here are three fundamental bond ladder ideas that you should understand before investing in addition to these steps:

1. Rungs

Your bonds are the ladder’s rungs. Divide the total amount you want to invest by the number of years you want the ladder to last to get the number of bonds you need for your portfolio.

Your portfolio will be more diversified and you will take on less risk as you have more rungs. Remember that minimum bond purchases typically range between $1,000 and $5,000. Your interest payments will increase as your investment amount does.

Take the total amount you intend to invest with the intention of making the ladder as long as you can. For instance, ten investments of $10,000 each could be made with $100,000 to purchase individual bonds.

The ability to build a ladder that will produce income each month of the year is another advantage of having at least six rungs.

2. Spacing

The distance between each rung’s height and the maturity dates of your bonds is represented. Every few months to several years is a possible range for this.

The majority of experts advise keeping the distances about equal. Due to the higher coupon rates offered by longer-maturity bonds, longer ladders typically result in higher income.

Shorter ladders may lower the bond ladder’s average return, but they also increase liquidity and lower reinvestment risk. Design your ladder with points of maturity every few months if you have short-term savings goals or believe you may need to access the funds in the near future.

3. Materials

The types of bonds you decide to invest in are the materials you use to construct your ladder. You want to find dependable, top-notch bonds, just like with a real ladder. Additionally, it’s crucial to choose bonds that the issuer cannot call early.

You can make decisions using Moody’s and Standard and Poor’s ratings, but you should also conduct your own research. Treasury bonds have a credit guarantee and municipal bonds may offer tax benefits, but corporate bonds typically offer higher yields.

Just keep in mind that not all bonds with the highest yields are the best. To diversify your portfolio, choose at least 10 different securities.

Types of Bond Ladders

Bond funds, ETFs, and individual bonds can all be used to build bond ladders.

Flexible individual bonds are available. You can choose the timing of maturity as well as the length of maturity, or the “height of the ladder.”

However, it can be challenging to manage credit risk, which is the risk that the bond issuer won’t honor its coupon obligations or return the principal at maturity.

If you decide to build your ladder out of corporate bonds, your ability to diversify the portfolio may be constrained by the amount of money you have to invest.

Bond ETFs with a maturity feature, like the Black Rock iShares iBonds or the Invesco Bulletshares, can also be used to build bond ladders. Bonds in the portfolio of these ETFs all have simultaneous maturities.

When the investment reaches maturity, the shareholders receive the proceeds, which they can then reinvest. Bond ETFs can diversify a portfolio for low-investment requirements. Since ETFs are traded on stock exchanges, they are also typically more liquid than individual bonds.

Pros and Cons of Using a Bond Ladder

Pros of Using a Bond Ladder

In order to manage cash flow and reduce risk exposure, investors can use the ladder strategy. Regardless of the current interest rates, it will eventually pay off. Keep in mind the following three advantages:

1. The flexibility offered by bond ladders

Bond ladders offer regular access to assets, which is probably their biggest advantage for novice or more cautious investors.

Regardless of whether you have bonds that are due to mature every month, quarter, or year, you can always choose whether you want to extend the ladder by reinvesting the principal into a new, longer-term bond.

Given the new credit and interest rate environment, you could also invest in various vehicles. There won’t be any consequences if you need to use the money for different costs.

2. Bond ladders generate dependable income streams

Bond ladder gains are remarkably predictable compared to other investments. You are aware of the amount and timing of the coupon payments you will receive along the way, as well as the fact that you will receive your principal back when the bond matures.

This consistency makes it simpler to create a budget and keeps you from unexpectedly or needlessly using up your savings.

3. Bond ladders mitigate the effects of changing interest rates

You can avoid being shackled to a single interest rate for a number of years by staggering points of maturity. You can modify your investments as various bonds mature based on the market.

You can reinvest more money if interest rates have gone up. Even if rates have decreased, you may still have bonds that are locked in for a longer period of time at a higher rate. Inflation reduces the value of fixed payment returns, and laddering provides protection against this.

Cons of Using a Bond Ladder

Bond ladders appear to be a low-risk, consistently yielding investment, but they do have some disadvantages. Here are two drawbacks to think about:

1. Bond ladders perform best when a sizable upfront investment is made

Bonds have a higher point of entry than funds because laddering necessitates purchasing multiple bonds at once, and most bonds are issued in $1,000 denominations.

Although it’s not required, investment professionals only advise creating a bond ladder if you have at least $100,000 to invest. Otherwise, the ladder will be too short or the rungs will be too widely spaced.

You might want to buy even more if all you’re investing in is corporate bonds. The higher default risk will be partially offset by greater diversification.

2. Bond ladders don’t completely eliminate risk

No investment can be guaranteed in full. The creditworthiness of the organization or company issuing the bond determines its value. They might give in.

Additionally, bonds may be called early, in which case the principal and interest payments stop. This can affect your ladder schedule and restrict your options for reinvestment in addition to lowering overall yields.

By diversifying your portfolio with only highly rated securities, you can reduce these risks, but some risk will still be present.

6 Things to Consider Before Building a Bond Ladder

1. Understand your limitations

If you want to maintain adequate portfolio diversification and can spread your assets across a variety of bonds, consider asking yourself—or your advisor—if you have enough money to do so.

Since bonds are frequently sold in minimum quantities of $1,000 or $5,000, you might need a sizeable investment to achieve diversification.

If you intend to invest in individual bonds that have a credit risk, such as corporate or municipal bonds, it might make sense to have at least $350,000 allocated to the bond portion of your investment mix.

Consider a Treasury or CD Ladder for smaller amounts because the credit risk is greatly decreased.

Ensure that you have enough cash on hand to cover both your needs and any emergencies. Also think about whether you have the time, desire, and investment know-how to research and manage a ladder or if a bond mutual fund or separately managed account would be a better option for you.

2. Employ top-notch bonds

Utilizing riskier, lower-quality bonds is counterproductive because ladders are designed to deliver predictable income over time. Ratings are a good place to start when looking for bonds with higher quality.

Pick only bonds with a “A” rating or higher, for instance. However, ratings can change, so you should conduct more research to make sure you’re comfortable investing in a bond you might end up holding for years.

More issuers are needed to diversify your ladder if you are investing in corporate bonds, especially lower-quality ones.

3. Keep bonds until they mature

The ability to weather the ups and downs of the market requires a certain temperament. For the purposes of maximizing the advantages of regular income and risk management, you must hold the bonds in your ladder until they mature.

You run the risk of losing money if you sell too soon, and transaction costs are also a possibility. If you are unable to hold bonds until they mature, you might encounter interest-rate risk comparable to that of a bond fund with a similar duration, which you might want to think about instead.

4. Don’t place callable bonds on your ladder

Knowing when you will receive interest payments, when your bonds will mature, and how much you will need to reinvest are all appealing aspects of a ladder. But if a bond is called before it matures, the interest payments stop and you receive your principal back, possibly against your will.

5. Consider the timing and frequency

The amount of time a ladder spans and how frequently bonds mature and pay back principal are two additional characteristics.

Although a larger investment is necessary, a ladder with more bonds will offer a wider range of maturities. You will have more opportunities to be exposed to changing interest rate environments if you decide to reinvest.

6. Refrain from investing in the bonds with the highest yields

A bond’s unusually high yield in comparison to other bonds of a similar type frequently means that the market is expecting it to be downgraded or believes it to be more risky than other bonds, and as a result, has driven down its price and raised its yield.

One possible exception are municipal bonds, where buyers frequently pay more for well-known bonds and bonds from smaller, but still reliable, issuers that may offer higher yields

What Bond Ladder Means for Investors

Bond ladders are an investment, just like any other. Bond ladders frequently have long durations, which means that if interest rates rise, their value could decrease significantly. But if investors stick to the plan and hold bonds until maturity, market fluctuations might not matter.

A long-term investment strategy for income and capital preservation is bond ladders. A bond ladder might make sense for you if you are close to retirement or have other needs for dependable investment income.

How Ladders Might Be Useful in Times of Rising Rates

A ladder may be helpful when yields and interest rates are rising, which will likely continue through the end of 2022 at the very least, according to the Federal Reserve.

The reason for this is that it regularly frees up space in your portfolio so you can benefit from new, higher rates in the future. Your ability to reinvest at higher yields may be limited if all of your money is in bonds with a single maturity date because your bonds may also mature before interest rates rise.

The timing of the reinvestment is spread out with a bond ladder framework, in contrast, as bonds mature at various intervals into the future.

By guaranteeing that bondholders will receive the full principal amount when the bond matures and assuming that the issuer will continue to operate and be able to repay its debt as it becomes due, ladders can also provide some protection from the possibility that rising rates could cause bond prices to decline.

How Ladders Might Be Useful in Times of Falling Rates

Bond interest payments can help you make money until the bonds mature or the issuer calls them. Because rates and yields frequently fluctuate, there is no assurance that you will find new bonds paying a comparable interest rate when that time comes.

You can potentially spread this risk across a number of bonds by laddering bonds with different maturities. Even if one of the bonds in your ladder matured as yields were declining, the longer-dated bonds in your ladder would still be earning interest at the higher older rates.

Pained by financial indecision? Want to invest with Adam?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.