Adam Fayed In The Media

Reuters announcement on Africa and Singapore push

SINGAPORE, June 9, 2025 (EZ Newswire) — British financial entrepreneur Adam Fayed, opens new tab has announced a push across East and West Africa, with plans to

SINGAPORE, June 9, 2025 (EZ Newswire) — British financial entrepreneur Adam Fayed, opens new tab has announced a push across East and West Africa, with plans to

We are looking for businesses to buy, in the financial services industry.

I am delighted to announce that I have re-released my 2018 Amazon book…..completely for free! The updated 2024 version includes answering questions such as: The

What makes me different, and how does that benefit you?

Gain your free expat financial and investing guides today

What are the 6 biggest reasons for expats and HNWI to have an advisor?

Recent client case studies

I am happy to announce my 34th LinkedIn review

adamfayed.com on Forbes – I am delighted to announce that I will soon be a regular contributor for Forbes.com

Many expats assume Mexico is cheap and overlook tax friction and jurisdictional risk. Mexico is affordable, yes, and an expat in Mexico can live comfortably on

Financial planning for expats in Colombia means managing banking, taxes, budgeting, investments, and retirement across borders. Most expats worry about currency fluctuations and inflation. That’s

US expats in Colombia must file an FBAR (FinCEN Form 114) if the total value of their non-US bank and financial accounts exceeded 10,000 USD

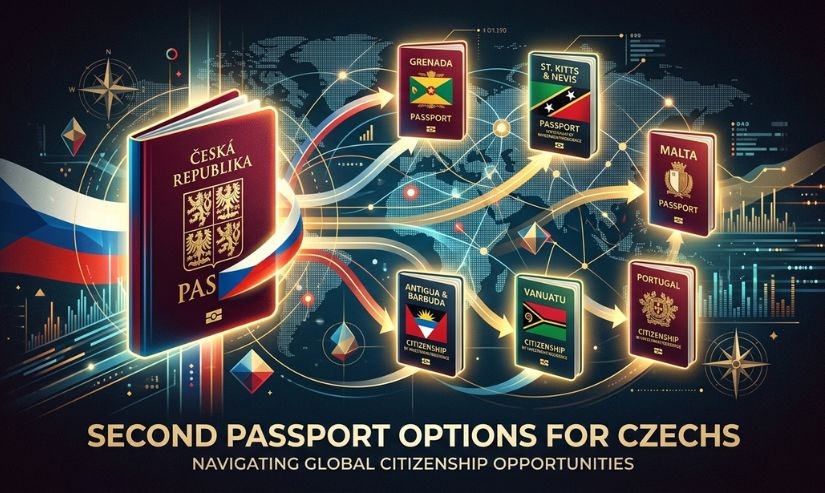

A second passport for Czechs typically involves global programs like Portugal, Turkey, Caribbean citizenship-by-investment options such as Grenada or St. Kitts and Nevis, and South

A second passport for Bulgarian citizens is typically pursued through diversification-focused options like Paraguay, Uruguay, and selective Caribbean programs such as Grenada, offering advantages that

Polish citizens can obtain a second passport through countries such as Portugal, Turkey, and select Caribbean nations without losing their Polish citizenship. A second passport

A second passport for Ukrainians is now legally possible with approved countries such as United States, Canada, Germany, Poland, and Czech Republic under Ukraine’s new

The best second passport options for Bangladeshis include Turkey, Portugal, and Caribbean citizenship-by-investment countries like Dominica and St. Kitts and Nevis, combining fast-track citizenship options

MCB Private Banking is among the established private banking providers in Mauritius, offering discretionary portfolio management, multi-currency banking, and access to a regulated offshore financial

The market and investment outlook for second-quarter 2026 (Q2 2026) highlights macro conditions such as inflation, interest rates, and geopolitical risk, but portfolio outcomes hinge

Q2 2026 investment outlook is defined by a fragile balance between rising energy-driven risks and markets that remain unusually calm. Navigating this environment means understanding

A second passport for Taiwan refers to practical citizenship pathways such as Caribbean CBI programs for speed, Turkey for investment access, or European residency routes

A second passport for China is not recognized under Chinese nationality law because China does not allow dual citizenship. In practice, Chinese citizens who acquire

The best second passport for Somalis includes Turkey, Caribbean citizenship-by-investment countries like St. Kitts and Nevis and Dominica, and European residency pathways such as Portugal

A second passport for Iraq typically involves citizenship options such as Caribbean investment programs like St. Kitts and Nevis or Dominica, Turkey through real estate

A second passport for Libyans typically involves citizenship pathways such as Turkey, Caribbean citizenship-by-investment schemes like Dominica and St. Kitts and Nevis, or European residency-to-citizenship

A second passport for Afghanistan citizens is most realistically pursued through residency and humanitarian pathways in countries like Germany, Canada, and Turkey, while investment-based options

A second passport for South Sudan citizens is most commonly obtained through Caribbean citizenship-by-investment programs such as Dominica and St. Kitts and Nevis. Countries like

A second passport for Iranians can be obtained through citizenship-by-investment and naturalization pathways, with options including St. Kitts and Nevis, Turkey, and Armenia, offering increased

Russian citizens can obtain second citizenship through citizenship-by-investment programs such as Turkey and Caribbean countries, or through residency-based pathways in Europe that lead to citizenship

A second passport for Pakistan citizens typically involves a choice between Pakistan-compatible countries like the United Kingdom, Canada, and Australia, or faster options such as