We will mainly discuss Dimensional Fund Advisors vs Vanguard in this article and touch on how the latter compares to iShares and BlackRock index funds. We will also answer some frequently asked questions, including what smart beta funds are in human terms.

If you prefer video content, the content below summarizes the article.

For those that are interested in investing you can email me at advice@adamfayed.com or contact me here. That includes for people who want to diversify beyond Vanguard or Dimensional.

In the current market there are many assets that can beat a diversified portfolio of stocks and bonds.

The information in this article is for general guidance only. It does not constitute financial, legal, or tax advice, and is not a recommendation or solicitation to invest. Some facts may have changed since the time of writing.

Getting to Know Vanguard

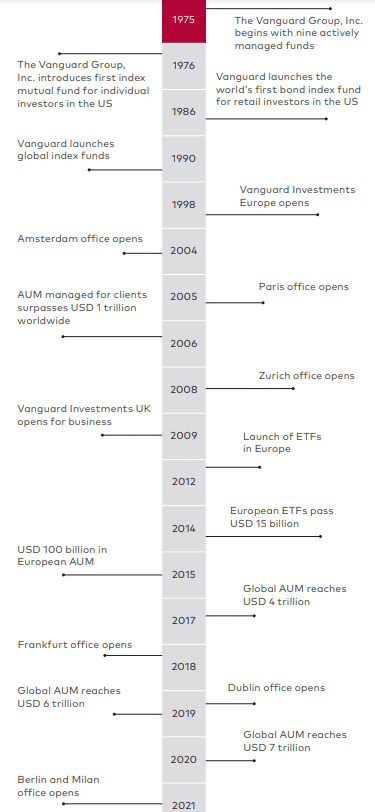

Vanguard Funds History

Many people know who Vanguard is. They are one of the biggest financial services groups in the world, with 7.6 trillion USD of global assets under management (AUM) as of Jan. 31, 2023.

Founded by the late Jack Bogle in 1975, they are most famous for their index funds which track a specific index, such as the S&P500 or MSCI World.

They do offer actively managed funds as well, although those funds have typically lagged their main index funds.

In the snapshot below, you’ll see a brief timeline of some key events in Vanguard’s history:

Vanguard Products and Services

Vanguard offers a comprehensive suite of investment products and services to help individuals and institutions achieve their financial objectives.

Vanguard Mutual Funds

One of Vanguard’s flagship products is their mutual funds, which are designed to track specific market indexes and provide a diversified portfolio of stocks or bonds at low costs. They offer both index funds and actively managed funds that seek to outperform their benchmarks.

Vanguard ETFs

In addition to mutual funds, Vanguard provides a variety of exchange-traded funds (ETFs) that offer exposure to equities, fixed income, and commodities. ETFs trade on an exchange like individual stocks and are also offered at low costs.

Vanguard Retirement Accounts

Vanguard also offers retirement accounts such as traditional and Roth IRAs, SEP IRAs, and solo 401(k) plans that help individuals prepare and save for their retirement while potentially reducing their taxes.

Vanguard Brokerage Services

For investors who want to buy and sell individual securities, Vanguard’s brokerage services offer access to third-party research and tools to make informed investment decisions.

Vanguard Financial Planning Service

The firm also delivers financial planning and advice services, including portfolio management, asset allocation, retirement planning, and tax planning.

Vanguard Institutional Service

Investment management services are given to institutional investors, including endowments, foundations, and pension funds, with a focus on portfolio management, investment consulting, and risk management.

Getting to Know Dimensional Fund Advisors

Dimensional Fund Advisors Background

Less people have heard of investment management company Dimensional Fund Advisors LP (DFA).

Headquartered in Texas and founded in 1981 by David Booth and Rex Sinquefield, the firm focuses on investing in a broad range of stocks that are tilted towards small-cap and value factors. Such have historically been shown to generate higher returns over time.

DFA’s funds are only available through financial advisors and institutional clients, and the company has developed a reputation for working closely with its clients to create customized investment solutions that meet their specific needs.

They have 584 billion USD in firmwide assets under management as of Dec. 31, 2022. With offices in 14 different locations globally, they are fast growing. However, in terms of size, Vanguard is still much bigger.

Dimensional Fund Products and Services

DFA’s investment products include mutual funds, exchange-traded funds (ETFs), and separately managed accounts. The company offers a range of equity and fixed income funds that are designed to provide exposure to specific market segments, such as small-cap, value, and emerging markets stocks.

DFA’s mutual funds and ETFs are only available through financial advisors and institutional clients, and the company works closely with its clients to create customized investment solutions that meet their specific needs.

The company’s investment strategies are designed to help investors achieve their long-term financial goals, while also managing risk through broad diversification and systematic rebalancing.

In addition to its investment products, DFA provides a range of research, education, and support services to its clients. The company conducts extensive research on financial markets and investment strategies, and it regularly publishes articles and whitepapers on its findings.

DFA also offers a variety of educational resources to help investors understand its investment philosophy and approach, including seminars, webinars, and online resources.

Dimensional Fund Advisors vs Vanguard: How similar are they?

Both Vanguard and Dimensional Fund Advisors are investment management companies that offer a range of mutual funds and other investment products to individual and institutional investors. They have a strong reputation in the industry and are well-known for their low fees and investor-focused approach. They also place a strong emphasis on long-term investing and encourage investors to maintain a disciplined investment strategy.

Product Offerings

Vanguard offers a range of mutual funds and ETFs that track major market benchmarks, as well as actively managed funds that seek to outperform those benchmarks. In contrast, Dimensional Fund Advisors offers a range of mutual funds and ETFs that are designed to provide exposure to specific market segments, such as small-cap, value, and emerging markets stocks.

Availability

Vanguard’s products are widely available to individual investors through its website, as well as through a range of third-party brokerages and financial advisors. Dimensional Fund Advisors’ products are only available through financial advisors and institutional clients. The company also works closely with its clients to create customized investment solutions that meet their specific needs.

Investment Approach

Vanguard’s investment idea is based on low-cost, passive investing. The company believes in investing in broad market index funds that track the performance of major market benchmarks such as the S&P 500, with a focus on minimizing costs and taxes.

In contrast, Dimensional Fund Advisors’ investment idea is based on the efficient market hypothesis, which posits that markets are generally efficient and that it is difficult to consistently outperform them through stock picking or market timing.

Instead, DFA seeks to capture higher expected returns by investing in a broad range of stocks that are exposed to certain systematic factors, such as small size, low relative price, and profitability. These factors revealed higher yields in the long term.

Do note that both Vanguard and Dimensional Fund Advisors are known for their passive investing strategies, although there are some differences in the way they implement these strategies.

The main difference is that DFA focuses more on value and small caps, and claim to use superior technology.

This is sometimes known as a “smart beta ETF” or index funds. It follows an index so it is passive but also considers many factors in picking stocks within the index.

Before our probe into smart beta, let’s first discover active and passive investing.

Active Investing

Active investing is an approach in which an investment manager tries to beat the market by selecting individual securities that they believe will outperform their benchmark. The goal of active investing is to generate higher returns than the market average.

However, active investing can be expensive due to the research and management costs associated with it, and it is often difficult to outperform the market consistently over time.

Traditional fund managers (“active managers”) try to beat the stock market by picking specific stocks or sectors that will outperform – they are seeking alpha.

In other words, they charge you more than index funds to try to beat the index.

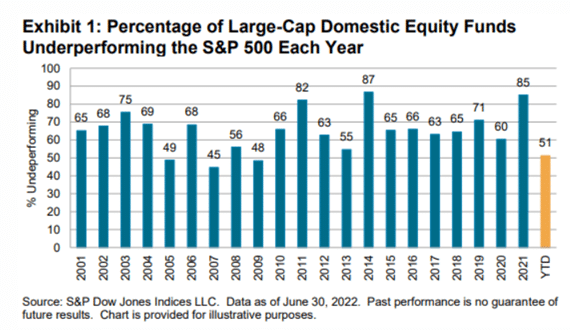

Most active funds have historically failed in this mission, at least in the long term. Many active managers can, and do, beat the S&P 500 over a 2- or even 5-year period but struggle over 20 years or more.

In 2022, active managers experienced their “best underperformance,” according to S&P Dow Jones Indices. This was because only 51% of large-cap active managers trailed the S&P 500 in the first half of 2022, which is significantly lower than the 68% average underperformance since 2009.

“Historically, beating the benchmark is very tough,” Anu Ganti told CNBC. Ganti is Dow Jones’ senior director for index investment strategy.

“And finally, we’ve seen the recovery in value after decades of underperformance,” Ganti said.

Passive Investing

Passive investing is an approach in which an investment manager seeks to replicate the performance of a market index or benchmark by investing in a representative sample of the securities that make up that index. The goal of passive investing is to achieve broad market exposure at a low cost, without trying to outperform the market.

Passive ETFs have gained popularity in recent years due to its low costs and the growing evidence that many active managers fail to outperform their benchmarks over the long term.

In comparison to active funds, index funds or passive investment funds, are merely trying to get the market average – a small cost for getting access to that fund.

What is Smart Beta then?

Smart Beta, on the other hand, is somewhere in the middle. It is a hybrid of active and passive investing that seeks to capture higher expected returns by investing in securities that exhibit certain systematic factors or “betas,” such as value, momentum, low volatility, or quality. Smart beta strategies use rules-based methods to select securities based on these factors, rather than relying on individual security selection.

Smart beta strategies are intended to offer the potential for higher returns than traditional passive investing, without the higher costs associated with active management. It is also relatively cheap like the passive funds but isn’t quite as passive as pure index investments.

However, they are different in that it uses computer algorithms to try to take advantage of market inefficiencies. So, it’s basically beating the market not from the human touch but with technology.

Advocates of smart beta claim it is the best of both worlds: the low costs of passive funds with the brains of an active fund.

In addition, supporters of these funds claim that smart beta gives investors a better risk-adjusted performance. In case they won’t always beat the market, they will give you a better performance relative to the volatility of the fund. In other words, they might fall less when the general market is down.

Another argument is that the US market is very weighted in favor of the biggest firms by capitalization, such as Apple, Amazon and Netflix, that have super high valuations.

So according to proponents of smart beta, they can add value by strategically picking, weighting, and rebalancing the stock picks that are built into the index.

So, it isn’t a purely weighted index fund and this can reduce risks.

Nevertheless, they are not without their own dangers and drawbacks, and their performance can vary depending on market conditions.

Because of this, there is a discernible difference between Vanguard and DFAs, as opposed to index funds like iShares, BlackRock, and others that frequently offer performance and fee structures that are nearly comparable to Vanguard’s.

DFA typically charges 0.15% extra for the funds annually versus Vanguard or iShares.

Do these differences affect Vanguard and dimensional fund advisors performance?

DFAs haven’t been around for a long enough time to make any concrete conclusions. In another 30 years, we will have a better idea about the reality of their claims to offer over-performance.

However, in the last 10-12 years, Vanguard has often beaten dimensional fund advisors performance marginally. Even where DFA has come out on top, the difference is marginal, and only for a few years.

| Year | Index – Benchmark | DFA Large Cap | Vanguard S&P |

| 2019 | 27.6% | 27.59% | 27.56% |

| 2018 | -4.38% | -4.43% | -4.42% |

| 2017 | 21.83% | 21.73% | 21.78% |

| 2016 | 11.96% | 11.90% | 11.93% |

| 2015 | 1.38% | 1.38% | 1.35% |

| 2014 | 13.69% | 13.53% | 13.63% |

| 2013 | 32.39% | 32.33% | 32.33% |

| 2012 | 16.00% | 15.82% | 15.98% |

| 2011 | 2.11% | 2.10% | 2.09% |

| 2010 | 15.06% | 15.00% | 14.91% |

| 2009 | 26.46% | 26.62% | 26.49% |

Take the DFA US Large Company Portfolio, which is similar to the S&P500 Vanguard Index. As per the stats below, DFA has beaten Vanguard some years, and trailed during other periods:

In some ways as well, the above figures are not a completely fair example because the DFA fund tilt their focus to small caps, which have done better long term.

In recent years, the performance of small-cap and large-cap indices has been mixed.

So DFA large cap vs Vanguard S&P 500 isn’t an exact apples vs apples comparison. It is more like apples vs apples and with some oranges in the same basket!

If we extend the category search to small caps, international large caps, and other categories of funds, we find that Vanguard slightly beats DFA with lower expense ratios and also lower volatility.

Hardly a huge advantage, but it does show that beating Vanilla index funds isn’t easy on a consistent basis.

Don’t small caps usually beat large caps?

Small caps have beaten large caps over the last 100 years; however, it depends on which time horizon you pick.

For example, small caps drastically beat large caps in the Great Depression, but have also trailed large caps during other periods.

What are the upsides and downsides of investing in Dimensional Fund Advisors vs Vanguard?

Here are some of the potential pros and cons of investing in Vanguard and Dimensional:

Vanguard Pros

- Low Costs: Vanguard is known for its low expense ratios and is often seen as a leader in the low-cost investing movement.

- Diversification: Vanguard offers a wide range of funds that provide exposure to various asset classes, allowing investors to build diversified portfolios.

- Passive Investing: Vanguard’s funds are designed to track market indices, which can be beneficial for investors who want broad market exposure without the risks of active management.

- Accessibility: Vanguard’s funds are widely available, making it easy for investors to access them through financial advisors or directly through Vanguard.

Vanguard Cons

- Limited Customization: Vanguard’s passive investing approach means that investors have limited control over their investment strategy, which may not be ideal for some investors with specific goals or preferences.

- Market Volatility: Vanguard funds are designed to track market indices, which means that they will experience market volatility, potentially leading to significant losses during market downturns.

DFA Pros

- Factor-Based Investing: DFA’s investment strategy is based on academic research and focuses on factors that have been shown to drive higher returns over time.

- Access to Premium Factors: DFA’s funds offer exposure to premium factors like size, value, and profitability that have historically generated higher returns.

- Diversification: Like Vanguard, DFA offers a range of funds that provide exposure to various asset classes.

DFA Cons

- Limited Availability: DFA funds are primarily offered through financial advisors, and not all advisors have access to them, limiting accessibility for some investors.

- Higher Minimum Investments: Many DFA funds have higher minimum investment requirements compared to some other mutual funds or ETFs.

Frequently Asked Questions

This section will answer some frequently asked questions (FAQs) that haven’t been covered already in the article.

Can you buy dimensional fund advisors online?

You can’t currently DIY invest DFM (discretionary fund manager) investments. You need to go through an advisory firm. The reason is to stop “hot money” coming in and out, like what happened to Vanguard in 2009 and during previous stock market crashes.

DFM want people to buy and hold, which they assume is more likely to happen through advisory firms.

There is certainly some degree of truth to this statement. Various studies have shown that investors that are in index funds still try to time the markets.

This contributes to results like the ones below:

I have personally lost count of the number of people I have met, that have stopped investing due to Trump, Brexit and various other political events.

How about Vanguard in comparison to iShares and other index funds?

What is most interesting is, if we compare Vanguard with iShares ETFs, the performance is also very similar. The same is true with BlackRock or HSBC (UK) index funds.

Ultimately most index funds these days are relatively similar, with the exception of these “smart beta” ones like from DFA.

So, investing with Vanguard over iShares won’t give you a huge advantage.

What does Jack Bogle think about smart beta?

The father of low-cost investing Jack Bogle, was unimpressed before his death with the idea that Vanguard, Dimensional Fund Advisors, or any other firm, could beat the traditional index fund with smart beta tactics.

He commented that value and small caps will outperform during certain periods of time, but that doesn’t make over-performance over the long term likely.

If smart beta is winning, dumb beta is losing by the exact same amount. Meaning strategy A might work for investor A, but strategy B might not work for investor B.

What is most interesting about Bogle’s analysis is that he contended that these funds don’t help improve risk-adjusted performance in the long term – one of the key arguments proponents of smart beta use.

Vincent Deluard, global macro strategist for INTL FCStone, also had some strong arguments, as per the video here. As he mentioned, specific smart beta funds can outperform for a short period, but that isn’t a good reason in isolation to invest.

What does Beta measure?

Beta measures the volatility of an asset. For example, if the S&P500 is used as proxy, the beta is one.

A stock that has a beta of 3 has a return which changes by three times as much as the general market – whether positive or negative.

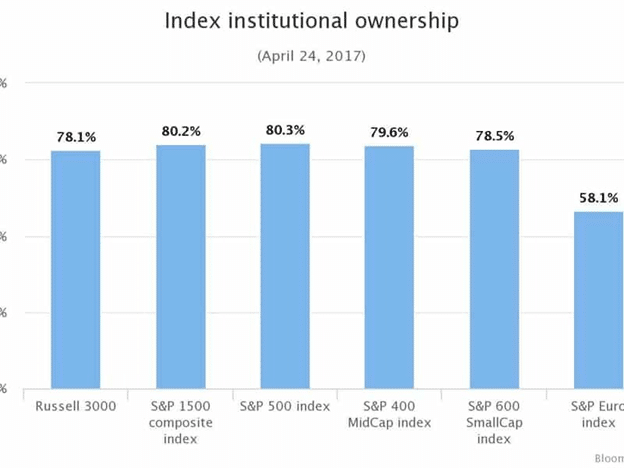

Why is it easier to beat a small cap index than the S&P 500?

The S&P 500 is mainly institutional money. That wasn’t the case in the 1950s or 1960s when the average investors were teachers, doctors and other individuals that often traded on emotions.

Now most owners are institutional – including banks and hedge funds. Small caps, especially in emerging markets, have less institutional investors.

That doesn’t mean in the US and UK the small cap indexes are vastly different to the larger markets like the S&P500.

Small cap indexes has been driven by institutional money as the 2017 graph below shows, which is still true to this day.

So, beating a small cap index might be slightly easier than a large cap one but has also gotten more difficult.

This trend has also lead to a situation where even great investors, like Warren Buffett, are struggling to beat the market.

Are most smart beta funds alike?

Not all smart beta funds are the same. Dimensional Fund Advisors is just one option.

Each smart beta fund has its own methodology, bias and smart beta index to track, so they can vary significantly in terms of their investment objectives, underlying rules, and portfolio holdings.

For example, one smart beta fund may aim to generate higher returns by investing in companies with strong fundamentals, while another may focus on companies with low volatility or high dividend yields. Some smart beta funds may track a single factor, such as value or momentum, while others may track a combination of multiple factors.

Are these a bubble?

I have written elsewhere to be cautious about this hype surrounding bubbles. Neither of these investment strategies has reached bubble levels yet.

How about performance during the 2020 bear market?

Many of the large caps have global revenue like Amazon, Netflix and Apple, and are better suited at adapting to a remote and digital world. In fact, Netflix and some of the large caps had seen increased revenue, as more people stayed at home during the lockdowns.

Dimensional Fund Advisors vs Vanguard: Final Verdict

There are many good things about some of these smart beta funds, including dimensional fund advisors.

It is true, for example, that the statistics show that DIY investors in Vanguard and iShares, lose to the general market they are tracking. They, all too often, buy high and sell low.

The fact that DFA only accept through advisors might place a check and balance against this.

There isn’t enough evidence yet, however, to ascertain that DFA are a superior way to invest. They have thus far failed to beat Vanguard, iShares and other index funds.

They are good funds, but that doesn’t mean the technology will help you beat an iShares or Vanguard Fund.

Overall, the choice between Dimensional Fund Advisors vs Vanguard ultimately depends on your individual needs and preferences. Vanguard may be a good choice if you’re seeking a low-cost, passive investing strategy, while Dimensional Fund Advisors may be a better fit if you’re looking for a more active, evidence-based approach.

However, it’s important to note that past performance is no guarantee of future results, and you should carefully consider their own risk tolerance and investment goals before choosing an investment strategy.

In reality, whether you buy a Vanguard, iShares, BlackRock or HSBC fund (for UK investors) really won’t make much difference in terms of performance.

The key things are investing for the long term, how much you invest, and asset allocation.

So, for now I would avoid the hype surrounding “smart beta ETFs.”

Even if they have a slight chance to outperform long term, my money would still be on a tiny over-performance for more vanilla Vanguard and iShares index funds.

If you are curious, you could try having a small allocation linked to DFAs and see how they perform relative to Vanguard long term.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.