Quilter Cheviot, also known as Quilter Cheviot Investment Management, is a Discretionary Fund Manager (DFM). It is currently owned by one of the largest players in both the UK and offshore expat financial arena (Old Mutual), and also have its own fund ranges.

Quilter Cheviot has 24.9 billion pounds or around 30 billion US dollars assets under management as of September 30, 2022, and this number keeps increasing.

The discretionary fund manager has offices located in 13 different areas around the United Kingdom, in addition to having an international footprint in Jersey and Dubai. The firm provides a wide array of investment services and has a comprehensive offering. It is also used by some advisors in the expat arena.

In order to cater to more than 36,000 customers, Quilter Cheviot has designed investment solutions that are particularly suited to the client’s needs as well as their risk profile.

We will discuss the services offered by the firm and give our review alongside suggesting what you can do if you have a portfolio with the company.

If you are looking to invest, my contact details are hello@adamfayed.com and WhatsApp +44-7393-450-837.

The information in this article is for general guidance only. It does not constitute financial, legal, or tax advice, and is not a recommendation or solicitation to invest. Some facts may have changed since the time of writing.

What are Discretionary Fund Managers?

Increasingly, many expat financial companies are outsourcing the financial management to Discretionary Fund Managers (DFMs). So, the financial advisor is selecting the DFMs they recommend and then using them to select investments.

In this model, the advisor is simply doing the financial planning part of the operation, such as finding out how much money the client can afford to invest, but then is outsourcing the investment management part of the puzzle.

What are the options available with Quilter Cheviot?

Discretionary Portfolio Service

It is intended for people who would like to invest more than 250,000 pounds (300,452.5 dollars). With this account, an investment manager will have control over your holdings, will determine what you buy, sell, and when to take action based on their best judgment.

They will construct a portfolio for you that corresponds to your goals and will manage it actively, so they will make appropriate modifications according to changes in your tolerance to risks and investment time frame, as well as fluctuations in the market and the economy, plus other variables.

Your dedicated Investment Manager will not only manage your investment portfolio but will also serve as your point of contact and be available to answer any questions you might have. You will have regular scheduled meetings with them, but in addition to that, you will also have the ability to talk to them whenever you want.

Managed Portfolio Service

Individuals with an investment budget of more than 40,000 pounds (48,072 dollars) can take advantage of Quilter Cheviot’s Managed Portfolio Service (MPS).

You will have access to the following under this service:

- a local investment manager who is dedicated to addressing any concerns you may have regarding your portfolio

- a complete custody, portfolio administration, as well as detailed reporting services, such as valuation, capital gains tax report, tax-year end, plus online reporting

- the firm’s equity and fund research teams will provide you with factsheets per month on top of regular investment editorials.

Climate Assets Funds

Both the Climate Assets Balanced Fund and the Climate Assets Growth Fund make investments in businesses that are actively working to improve the state of the world while adhering to a set of core moral principles.

Investing in businesses that are dedicated to finding long-term solutions to some of the problems facing the world is a primary focus of this investment service. It also offers a solution to potential investors who are interested in investing in the expanding markets for sustainable practices and environmental technologies and those who possessed a balanced or growth risk appetite.

To guarantee that the firms is making well-informed decisions on its investments, the Climate Assets investing process takes into account a number of important aspects of sustainability and conducts data analysis.

Specifically, the focus for most of the investments are in these three areas:

- businesses that share the firm’s commitment to ethical principles

- government bonds that assist in providing portfolio protection

- non-traditional assets such as the infrastructure for renewable energy sources

This service also focuses on medium and large enterprises of high caliber, which have the potential to minimize the cyclical nature of returns and safeguard investments.

The investments made are solely in businesses that can provide answers to persistent problems within the following industries: water, food, clean energy, health, and resource efficiency industries.

Companies that make their money from dubious areas of the economy are not eligible for investment in the funds.

Climate Assets Balanced Fund

This fund was rolled out in 2010 as part of Quilter Cheviot’s Climate Assets Funds service.

The equity content under this fund is between 60% and 75%.

Climate Assets Growth Fund

This was recently rolled out, in 2022, and contains equity of between 75% to 95%.

You have the option of directly investing in the Climate Assets Balanced and Growth Funds, as well as investing through one of the following platforms: AJ Bell, Hargreaves Lansdown, Interactive Investor, and The Big Exchange.

AIM Strategy

Individuals who would like to invest more than 100,000 pounds can take advantage of Quilter Cheviot’s Alternative Investment Market (AIM) Strategy, which was developed with estate and inheritance tax (IHT) preparation in mind. Clients who have been introduced to the Quilter Cheviot AIM Strategy by a professional adviser are eligible to invest in the strategy.

The Quilter Cheviot AIM approach prioritizes the protection of capital while minimizing the impact of inheritance taxes. Investors have the opportunity to acquire access to a broad portfolio of companies that are listed on the Alternative Investment Market by participating in a tax-efficient elective approach.

Because it is anticipated that these enterprises will be eligible for Business Relief, the investor’s prospective inheritance tax liability may be reduced as a result of the investment in such businesses.

What are some of the benefits of utilizing the AIM Strategy?

Possible decreases in inheritance taxes

After two years, assets that have been invested in the AIM service will no longer be considered part of the investor’s estate and will therefore no longer be subject to inheritance tax. In other words, the beneficiaries are exempt from paying an inheritance tax of up to 40 percent of the fortune they received.

Wrappers for Individual Savings Accounts (ISA) can accommodate portfolios

Putting those assets inside of an ISA wrapper not only removes them from the reach of the Inheritance Tax, but it also protects them from the Income Tax and the Capital Gains Tax.

Management that is active

The investments of customers are actively managed within the AIM portfolio, and Business Relief is incorporated as an integral component of the approach.

Quilter Cheviot enjoys the benefits of having an in-house Small Cap expert that works to choose equities that generate cash, are profitable, and have healthy balance books. The company must take an active role in managing the portfolio to ensure that the stocks continue to satisfy the requirements that have been set.

Additionally, the company has access to both small and worldwide large cap corporations, which, along with the assistance of the company’s in-house specialized equities and funds analysts, provides a substantial amount of information.

What criteria are used to select companies?

The research department at Quilter Cheviot conducts a check on AIM-listed stocks that have a market cap of at least 250 million pounds and a free float that sits at a minimum of 50 percent. The percentage of a company’s shares that are freely tradable on the stock market is referred to as the “free float.

After that, this list is narrowed down to include only the stocks that are eligible for business relief. Due to these criteria, the list of stocks can be narrowed down to approximately 100. After compiling this prospective buy list, the team will perform in-depth research on the qualities of individual equities that are being considered for inclusion in the portfolio.

Considerations pertaining to the environment, society, and governance are completely incorporated into the research procedure, which assists in the identification and awareness of potential prospects and risks involved.

Business Relief was first implemented in the United Kingdom in 1976 with the intention of shielding certain qualifying business assets from inheritance taxes. This protection extends to a relief of one hundred percent for shares held in eligible unquoted trading enterprises. For the purposes of these considerations, unquoted shares include those quoted on AIM.

If the firm is eligible for relief and the asset is retained for a minimum of two years, the asset’s value is free from IHT upon the death of the investor, subject to possible constraints where the firm owns any excepted assets. Such excepted assets mean investment assets that are not considered necessary for the company’s operations.

The investee firms that are chosen to be included in your Discretionary Managed AIM Strategy will be under a recurring and independent assessment per year that will be conducted by tax specialists that Quilter Cheviot has retained.

During this assessment, the financial records of each investee firm are analyzed, and a description of the scope of the business relief that is likely to be made accessible to investors in that business is provided.

Investors ought to be aware that the final decision regarding whether or not the stocks meet the criteria for Business Relief will still be made by HM Revenue and Customs (HMRC) during probate and will be dependent on the particular situations of the investee firm during the time of the investor’s passing.

Are there risk controls implemented?

- Get to know the management before any investments are made.

- Steer clear of companies that consistently lose money.

- Steer clear of so-called blue sky firms

- at least 250 million pounds worth of market cap

- ownership of a firm’s free float should not exceed 3%

What about service costs?

The initial fee is 1% plus VAT, up to a maximum of 5,000 pounds.

This is calculated based on the total worth of the monies that were initially put into the strategy.

There is also a management charge of 1.25% per year plus VAT. The value of your portfolio at the conclusion of each month is used to calculate the yearly management fee, and this value is then averaged throughout the course of the charging period.

Within the context of the AIM Strategy, Quilter Cheviot does not impose any dealing charges on its customers. Because of this, clients can benefit from more accurate and open information regarding pricing.

What should you keep an eye out for?

When investing in smaller businesses, you must keep in mind that the risk involved is far higher than with investing in larger organizations.

Because there is a limited market for investments in smaller businesses, it may be more challenging to sell stakes in those companies.

The benefits of investing in this portfolio are contingent upon the regulations concerning taxes that are now in effect. Any potential future modifications to those rules could have an impact on any benefits obtained from holding onto AIM stocks.

It should be noted that the service is not suggested for any reason other than shielding assets from inheritance tax, and the only investors who stand to gain from it are those whose estates have a value that is more than the present level of IHT-free allowances, which is at 325,000 pounds.

Because the regulations governing business relief necessitates investments to be kept for a minimum of two years, in order to be eligible for inheritance tax relief, you should have kept investments in an eligible portfolio for a minimum of two years prior to your passing.

Advice & Dealing Service

Quilter Cheviot provides clients with access to a customized dealing facility that includes foreign stocks, fixed interest assets, and collective investments like unit trusts.

Through their Advice and Dealing Service, they are able to provide you with a significant amount of help even if you choose to take a more hands-on approach to the decisions regarding your investments.

What do you get when you use the Advice & Dealing Service?

- A devoted investment manager who is able to provide guidance, talk about specific investment concepts, and provide overall market summaries.

- Access studies on markets, economies, and currencies both in the UK and overseas.

- The services are provided by a stockbroking team.

If you would rather exercise your own investment choices and would like to be active in the everyday administration of your investment portfolio, there is a straightforward and commission-only method of trading that you may take advantage of too.

You will get contact to a dedicated investment manager as a feature of the service. This manager will be able to discuss specific investment ideas on top of more broad market observations, and there will be no additional management costs associated with this discussion.

Cash Management Service

Quilter Cheviot investors are urged to take a long-term strategy to investing, but it is also acknowledged that you might wish to retain funds for an emergency, a future plan, or just for convenience of access if you invest in the company. Therefore, in order to provide you with the opportunity to handle your financial matters online, they have formed a partnership with Flagstone.

What exactly is flagstone, then?

Flagstone is a web-based cash management platform that provides competitive interest rates available on a broad range of bank deposit accounts. It provides a straightforward method for managing funds while ensuring its growth at a predetermined rate for a period of time based on one’s choice.

Make sure to get in touch with an investment manager from Quilter Cheviot if you need assistance establishing and managing a Flagstone account.

You can obtain the highest possible rate of return by investing sums greater than 250,000 pounds for a variety of time frames, ranging from immediate access to five years through Flagstone.

Because the system is hosted online, it is incredibly easy to monitor both account balances and interest accrued around the clock.

The Financial Conduct Authority (FCA) regulates Flagstone and all of the banks that offer account opening services through the platform.

What are the fees and charges involved with Quilter Cheviot?

Quarterly Management Fee

There is a management fee that is assessed on a quarterly basis, and it is determined as a percentage of your portfolio. This encompasses all parts of portfolio management, including general administration, reporting, review meetings, and any costs associated with providing custody of assets, as applicable.

There are a few exemptions from the VAT that apply to the management fee, but it will be subject to VAT overall.

Annual Management Fee

There is a 1% standard fee per year that is calculated based on the portfolio’s entire valuation as of the end of each month, then averaged across the charging time frame and charged in arrears every three months. A VAT is also charged as applicable.

There is a possibility that the annual management fee would adhere to a tiered structure. This implies that the cost will decrease proportionately to the growth of the amount of money invested. In the event that a tiered structure is utilized, the Investment Proposal will provide specific information regarding its implementation.

Other Charges

ISA Initial Cost

There is a 0.50% preliminary fee for individual savings account on top of VAT, as applicable.

CHAPS Charge

There is a fee worth 20 pounds for every transfer under the Clearing House Automated Payment System (CHAPS).

SWIFT Charge

The cost for every transfer using the Society for Worldwide Interbank Financial Telecommunications (SWIFT) international payment network is also 20 pounds.

Currency Conversion Fee

After accounting for a foreign exchange brokerage fee of 0.07% from Quilter Cheviot’s broker, the exchange rate that is being used for currency conversions stands at 0.75%.

Custody Fee

There is a charge worth 45 pounds for every asset in the UK or abroad.

Dealing Commissions

The standard charges are:

- 1.90% on the first 10,000 pounds

- 0.50% on the succeeding 10,000 pounds

- and 0.30% subsequently, with a fee worth at least 50 pounds for every deal

Dealing Charge

The dealing charge is worth 40 pounds for every transaction.

There are also third-party brokerage charges like the one added for currency conversion.

The total fees will largely depend on how much your advisor charges and what platform is being used. The total net fees could exceed 2% or 3% if you factor in all the layers of charges.

Why might Quilter Cheviot investors lose to the market?

Quilter Cheviot try to use research to identify future trends. This is almost impossible to do, alongside beating the market, after the net fees.

There are so many unknown unknowns and known unknowns, that being able to “out-research” the market is almost impossible.

Even if you are able to beat the market gross, the net returns might be lower, adjusted for such charges. 80% of investors fail to beat the S&P500 over 5-year periods and around 98% of investors fail to beat it over 40 to 50 years.

Lower volatility and diversification, moreover, doesn’t always lower your risk.

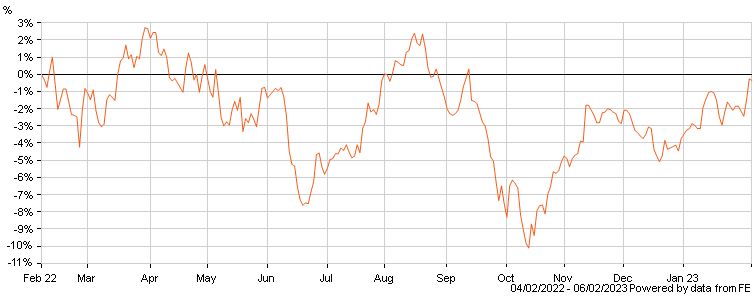

How about the performance during the 2020 bear market?

So far during the 2020 crisis, Quilter Cheviot multi-asset returns haven’t performed especially well, compared to a mixed portfolio of index and bond funds.

Their climate assets and Libero funds haven’t done well during the 2020 bear market.

Quilter Cheviot just like everybody else, couldn’t have seen such crisis coming, and markets are still recovering from its long-term impacts.

The point though is that it is hard to out-research the market by doing loads of research, if you live in a world with loads of unknown unknowns and known unknowns.

Quilter Cheviot Review: Conclusion

Quilter Cheviot is a professional company that have their fingers in many pies. Their funds aren’t bad, but they are not the best either. Many of their funds and investments have underperformed the market. Plus, there are so many charges that you can get a better deal out of elsewhere.

Take note that in investing, you must ask yourself these questions:

How much of a risk are you willing to take in order to make the progress you need toward your objectives?

It is essential to determine a level that you are content with, but keep in mind that this is something that can be modified as you progress through the many periods of your life.

What is the maximum amount of time you can commit to keeping your money invested?

Are you expecting to save for something with a longer time horizon, such as a pension, or do you require access to your money in the event of an unexpected emergency?

What exactly do you want to happen with the money you have invested?

You have the option of either progressively increasing your wealth, getting constant access to your investments, or a combination of the two. Should your goals shift, you are free to adapt your plan accordingly.

Discover if Quilter Cheviot is a strong option compared to Premier Trust, which we talked about in another post.

Pained by financial indecision?

Adam is an internationally recognised author on financial matters with over 830million answer views on Quora, a widely sold book on Amazon, and a contributor on Forbes.